©Bill & Melinda Gates Foundation/Prashant Panjiar

This blog presents an example of an existing livelihoods model to undertake a critical evaluation of how entrepreneurship is conceived for rural women in self-help groups (SHGs) in two parts. The purpose of this two-part blog is to show that the dominant construction of entrepreneurs as autonomous economic agents who move with, and towards, opportunities does not necessarily apply to our sample of rural SHG women in Chhattisgarh. Using data from an ongoing impact evaluation study, Part 1 describes the design and strengths of our livelihoods model, Haqdarshak, in improving incomes of SHG women who are trained in a mobile application for fee-based enrolment of community members in public welfare schemes. Despite the model’s obvious merits of skill training, efficiency in service delivery, and greater public awareness about entitlement programs, this piece initiates a discussion on how these "market-driven”, “competitive entrepreneurial” models are not rooted in an understanding of the normative risks that can impede women’s agency. No matter their level of engagement with Haqdarshak activities, SHG women are deeply rooted in, and give primacy to giving care. Part 2 in this blog series digs deeper into the normative environment that defines women's work, and the presence/absence of support systems at home and outside that affect women's agency and inform their decisions to achieve a work-life balance. Findings from our study have implications for the sustainability of the Haqdarshak model, and inform a set of policy recommendations for institutionalizing income-augmenting opportunities for rural SHG women.

Study Background and Data

Chhattisgarh, the site of our ongoing impact evaluation study that informs this piece, is a state in central India with the highest poverty rate in India (40 percent) with over 76 percent of its 26 million people residing in rural areas (NIPFP, 2016; SRDP, 2018; World Bank, 2016). Leveraging the state government’s initiative to distribute smartphones to about 3 million members of women’s collectives in 2018, our research explores the potential of a digital intervention as a sustainable livelihoods option for SHG women in 5 districts in northern Chhattisgarh. The technology in question is a mobile application called Haqdarshak that is pre-loaded with procedural details on close to 200 welfare scheme applications and documents/IDs of the state and federal governments.[1] This blog piece draws on the following data from our ongoing study – (i) Haqdarshak MIS data on 2244 active women covering a 20-month period since August 2019; (ii) in-depth interviews with 30 women; and (iii) a baseline survey with 1267 women. The next section describes our digital intervention, and evaluates its potential as an entrepreneurial model for women’s collectives. A research question associated with our study on facilitating citizens’ access to the welfare state via an agent-based model asks: what is the impact of technology on the income and asset accumulation among SHG-affiliated women agents?

Haqdarshak Model: Four Design Elements

The design of the Haqdarshak entrepreneurial model has the following key elements:

(i) Access to Information, Financial Instrument, and “Markets”

Haqdarshak is more than just a mobile application. It is a digital resource that provides easy and comprehensive information on the eligibility requirements, application submission procedures, and benefits associated with a wide range of government schemes and documents. The livelihoods aspect of this model entails a service fee that SHG women-agents can charge for screening eligible beneficiaries and enrolling them into relevant welfare schemes and government documents (to fulfill application requirements for schemes). In our study, the “marketplace” of eligible beneficiaries refers to the villages in which these SHG women reside. [2]

(ii) Skill Development

The Haqdarshak model complements the capacity building requirement of the NRLM program by offering intense trainings to SHG women on engaging schemes/documents-related features on the app. Therefore, the Haqdarshikas do not just acquire new information on welfare programs beyond what is already known via their SHG activities, but also continuously advance their knowledge and skills through learning-by-doing screenings and enrollments in their communities. As of April 2021, the MIS database shows that of the total 5078 SHG women who were trained in the mobile application, 71 percent passed the training as a necessary first step to becoming a Haqdarshika. Of these qualified women, 67 percent (n=2302) have used the app to enroll themselves and their families, as well as their neighbors in the communities into 139 welfare schemes and 18 scheme-related documents. With respect to the 33 percent non-users, findings from our Haqdarshika survey show that the leading cause of program drop-out relates to insufficient time for enrollment activities. This is hardly surprising, given that about 70 percent of the women are employed in full-time jobs in the SHG and affiliated networks as presidents, treasurers, book-keepers etc.[3] Recognizing the numerous demands on their time, women who have “dropped-out” have nevertheless learnt a skill that they can leverage to earn supplemental income per their convenience/circumstance. In fact, our survey reveals that 38 percent of these drop-outs undertake offline enrollments in their communities.[4]

(iii) Decision-making Autonomy

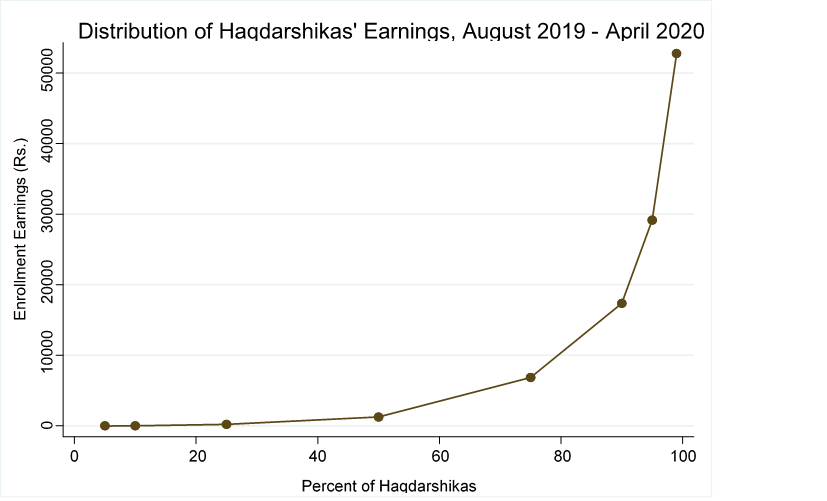

For each pre-installed welfare scheme or document on the mobile app, the Haqdarshika is also able to see a “government fee” and a total “service fee” that includes the former as well as a suggested processing fee for making applications. Since a Haqdarshika can evaluate the ease or cumbersomeness of the submission process (e.g., number of agents/agencies to be visited), the disaggregated fee structure allows her to decide how much (or, little) she wants to charge the citizens for processing their applications. Our data shows that, between August 2019 and April 2020, a Haqdarshika made an average of 117 welfare applications. However, the distribution is highly skewed to the right, being pulled by the top 20 percent of the Haqdarshikas who have remained active for at least 12 months (see Figure 1). Overall, these enrollment activities have generated a median income of Rs 1240 (or, US$ 17) per month, with the Haqdarshika’s income increasing by Rs 322 (or, US$ 4) for each additional month of work. To put these numbers in context, our survey shows that the median monthly income earned by a Haqdarshika at her primary job is about Rs 3000 (or, US$ 41).

(iv) Competition

Equipped with informational, technical, and financial know-how, the Haqdarshak model creates a cadre of service providers who can compete with other formal (paid) intermediaries like Bank Correspondents and community-level health workers like ASHA and Anganwadis. While the latter only provide information and/or application support for programs relevant to their department/agency, the Haqdarshak model assumes that the depth of coverage and on-the-spot earning opportunities spur creative decisionmaking (e.g., selecting schemes not targeted by rival agents) by their trained cadre of SHG women. Data shows that Haqdarshikas consistently target “high-value” schemes and documents (application fee ranging from INR 100 - 250) that sometimes don’t involve a government fee component. For example, health insurance schemes like Ayushman Bharat, Pradhan Mantri Jeevan Jyoti Bima Yojana, and Pradhan Mantri Suraksha Bima Yojana are free applications that together comprise just over 50 percent of the 143,432 applications made by the Haqdarshikas since August 2019.

Risk Exposure in Women’s Entrepreneurship

Despite its aforementioned merits, the entrepreneurial model lays no emphasis on, nor provides any tools/mechanisms to build or enhance the risk absorption capacity of the Haqdarshikas. The right-skew of the earnings distribution combined with the MIS data shows that 66 percent of the active Haqdarshikas have charged no fee for at least one application, thus exemplifying their exposure to economic risk -- the bedrock of entrepreneurship. The following representative quote highlights the predominant challenge in framing the Haqdarshak model as a market-driven livelihoods approach for rural women:

“I do not take money from people when I see their condition is very bad...how can I charge them? I make the document or scheme for them, and they say they will pay me later after receiving benefits. These people do pay me for my services.. mostly people understand that I am spending money for this service [filling out and submitting applications] so they pay me. But it’s not easy...people only trust when they receive benefits...”

(Interviewee NC5)

The above quote highlights how the socio-economic status of target populations and their past experiences with the welfare state impacts a Haqdarshika’s exposure to economic risk. Another risk condition that is often de-emphasized in entrepreneurship models is associated with “patriarchal risk” (Kabeer, 2015) manifesting in strained family relations due to volatility in women’s incomes and perceived dereliction of their caregiving “duties” by family members. As one woman noted:

“Initially their [family] response was good...they were happy and supportive of my work. But now they know I am not getting many applicants, so they are objecting and saying that I should leave this work [and that] I am wasting too much time and my house work is getting disturbed. I will do some other work. I am not happy like this…”

(Interviewee NC6)

Our findings recognize that women’s agency operates within the structural constraints of psycho-social norms and identities and intrahousehold distribution of assets and opportunities. Even as economic agents, women do not to see themselves as “autonomous” or detached from their relational roles within the household (see Cornwall, 2007; Leach and Sitaram, 2002). The next blogpost will argue for re-imagining entrepreneurship models for rural women by foregrounding how their relational roles act as critical conditions in unlocking the gains from community-based economic activities. Unsurprisingly, having a supportive family – e.g., a husband who participates in household chores, and digitally-literate children who help Haqdarshikas in making applications on the mobile app – is often a necessary condition for women’s engagement in Haqdarshak activities. Interestingly, it is the strength and density of a Haqdarshika’s social ties within and outside the SHG – e.g., relations with officials in other village organizations, local government, post offices and banks – that imparts “profitability” to this livelihoods model by reducing the economic costs associated with submitting the applications.

Endnotes

[1] The app is developed by a private company called the Haqdarshak Empowerment Solutions Private Limited (HESPL) who are partnering with us in implementing this digital intervention among SHG women.

[2] Upon completion of our study, these trained women-agents will be able to use the app to enroll citizens in other villages.

[3] Close to 30 percent identified agricultural labor and casual employment in public works as their primary economic activity.

[4] Qualified women who do not use the app within 15 days of getting their login credentials are deactivated in the MIS. The women can re-apply to renew their login ID for making enrollments through the app again.

References

Cornwall, A. (2007). Myths to live by? Female solidarity and female autonomy reconsidered. Development and Change. 38(1): 149-168

Kabeer, N. (2015). Women’s economic empowerment and inclusive growth: Labour markets and enterprise development. International Development Research Centre Working Paper. Available at: https://gsdrc.org/document-library/womens-economic-empowerment-and-inclusive-growth-labour-markets-and-enterprise-development/ (last accessed on May 17, 2021)

Leach, F. and Sitaram, S. (2002). Microfinance and women’s empowerment: A lesson from India. Development in Practice. 12(5): 575-588

NIPFP (2016). Madhya Pradesh: State MDG report 2014-15. National Institute for Public Finance and Policy Report. Available at: https://www.nipfp.org.in/media/medialibrary/2016/03/Madhya_Pradesh_State_MDG_Report_NIPFP_UNICEF.pdf (last accessed on May 17, 2021)

NRLM (2021). National Rural Livelihoods Mission website: https://aajeevika.gov.in/en/content/mission (last accessed on May 17, 2021)

SRDP (2018). State Rural Development Plan. Department of Panchayat and Rural Development, Government of Chhattisgarh. Available at: https://rural.nic.in/sites/default/files/EC_Meeting_ppt-final.pdf (last accessed on May 17, 2021)

World Bank (2016). Chhattisgarh: Poverty, growth & inequality. Available at: http://documents1.worldbank.org/curated/en/166551468194958356/pdf/105848-BRI-P157572-PUBLIC-Chhattisgarh-Proverty.pdf (last accessed on May 17, 2021)